Let me preface this post, by noting that I try to avoid writing about gold, since there are some many other excellent analysts out there writing about the subject. But when there is a such a strong overlap between gold and forex markets, well, I just can’t resist!

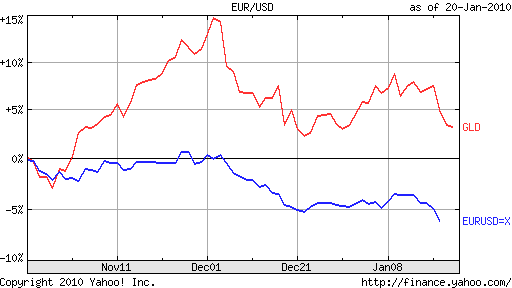

Recently, gold prices have collapsed at virtually the same rate as the Euro, with the result being a near-record high short-term correlation between EUR/USD and gold prices. This has caused no shortage of confusion among gold-watchers, which are accustomed to seeing the strongest (inverse) correlation with the US Dollar. This change is causing everyone to rethink some classically held assumptions about gold prices.

The foremost of which is that gold is chiefly a hedge against the Dollar, which is a symbol for inflation and erosion of value. [In fact, analysts argue that gold has little real purpose (besides a handful of trivial practical uses, such as jewelry), especially since holders of gold don't receive interest, there is little reason to own it other than as a store of value]. Thus, as the Dollar has declined over the last five years, gold has soared. Investors who are nervous about perennial budget deficits in the US and the skyrocketing national debt, have turned to Gold because of the belief it will continue to hold its value even (or especially) if the US government is forced to devalue its debt by devaluing the Dollar. While this tenet underlies the gold/Dollar inverse relationship, the long and short of it is that investors typically buy gold when the Dollar falls, and vice versa. Thus, when the credit crisis struck and the Dollar rallied, gold prices fell, despite the fact that the US was now more likely to default on its debt.

In the last month, however, the Euro has taken center stage in dictating the price of gold. This is most likely because of the sovereign debt problems of certain EU countries. A not insignificant number of which well exceed the budget (not to exceed 3% of GDP per year) and debt (not to exceed 60% of GDP) limitations imposed on them by their membership in the EU. Recent credit rating downgrades have underscored an increasing likelihood of default, which has been duly noted both by the forex and gold markets. As the Euro has dropped (quite dramatically in fact), so has gold.

According to the current paradigm, this is not wholly unsurprising, since the Euro’s fall has naturally been mirrored by a rise in the Dollar. Thus, if you continue to look at gold prices in terms of the Dollar, it seems naturally that a rising Dollar is being accompanied by falling gold. On the other hand, the fact that the Dollar is suddenly rising has little to do with a change in US fundamentals, and instead reflects the fact that in forex, it’s impossible to short all currencies simultaneously, even if sometimes fundamentals would justify such an approach.

In other words, that certain EU member states are more likely to default on their respective debt obligations has limited bearing on whether the US will also default. [If anything, it increases the likelihood, since a default in the EU would likely send sovereign borrowing costs higher around the world, straining the ability of the US to continue borrowing]. By extension, the current drop in the price of gold is fundamentally irrational, especially when viewed relative to currency markets. To borrow a hackneyed expression, perhaps it’s time for a paradigm shift.

No comments:

Post a Comment